Most owner-managed businesses don't have a cash forecast. They have a bank balance. The distinction matters more than most owners realize — usually around the time a payroll date and a large supplier invoice land on the same Friday.

The 13-week rolling cash forecast is the tool that closes that gap. It's not complex. It's not a CFO deliverable. It's a spreadsheet, updated weekly, that tells you where your cash actually is — not today, but in eight weeks.

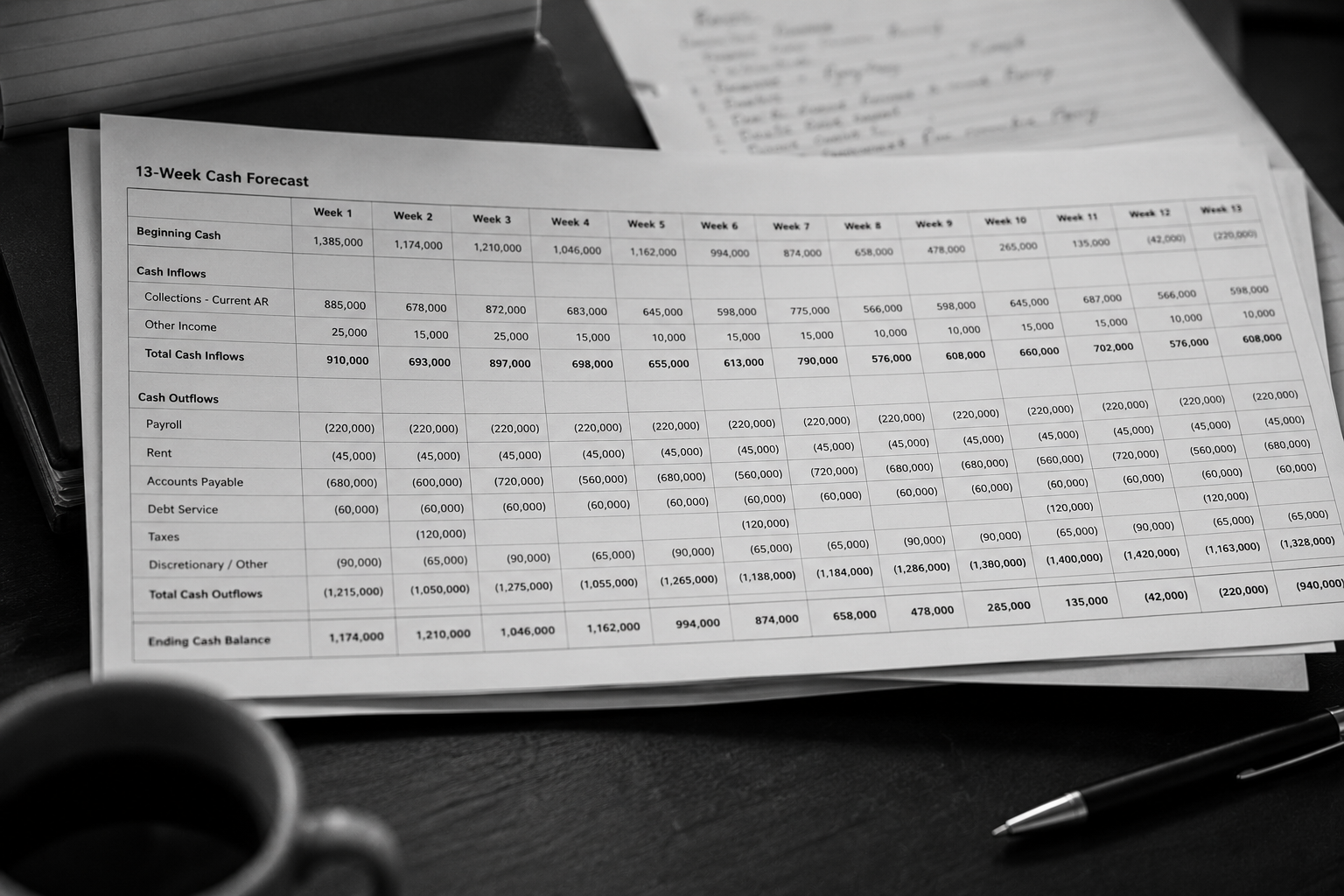

What a 13-week forecast actually is

Thirteen weeks is one quarter. Long enough to see most cash problems before they arrive; short enough to keep the numbers honest. "Rolling" means you don't reset it at quarter-end — you drop the week that just passed and add a new one to the front.

The inputs are simple:

- Opening cash balance

- Expected collections (from the AR aging, not from revenue projections)

- Known disbursements: payroll, rent, scheduled AP, debt service, taxes due

- Discretionary spend you can control if you need to

The output is a single column: projected end-of-week cash balance for each of the next 13 weeks.

The collections side is where most people hesitate. The right approach is to build it from your AR aging, not your revenue forecast. Look at what's actually outstanding, apply a realistic collection timing based on your history — "this client pays in 45 days, this one in 22" — and build a week-by-week schedule of when cash will actually arrive. Revenue projections tell you what you expect to invoice. AR aging tells you what you've already earned and when it's likely to land. For cash forecasting purposes, only the second number matters.

Why most businesses don't do it

The honest answer is that it feels like extra work. The books aren't fully closed, collections are lumpy, the timing of vendor payments shifts week to week. Building a forecast against moving inputs takes discipline the first few months, until the process is routine.

The second reason is that owners trust their instincts. They've run the business for years; they know roughly when money is tight and when it isn't. That works, right up until it doesn't — when a large client pays 30 days late and a capital expense converges with a quarterly tax installment in the same two-week window.

The third reason, less often admitted, is that the forecast sometimes shows something the owner doesn't want to see clearly. A bank balance is blurry. A 13-week model is specific. There's a certain comfort in not knowing the exact week things get tight — until that week arrives and the options have narrowed considerably.

What it changes

A current forecast doesn't just tell you when you'll run short. It changes the decisions you make before that point.

With 13 weeks of visibility, you can:

- Time a vendor negotiation against an expected surplus, not a crunch

- Push back on a customer's payment extension before accepting it

- Decide whether a hire or a capital purchase is actually affordable — not based on today's balance, but on the three-month picture

- Tell your bank something concrete when they ask how the business is performing

Without it, all of those decisions happen on instinct. Sometimes instinct is right. The problem is you don't know which times it isn't until after.

What to do when the forecast shows a gap

This is the part that actually matters. A forecast that shows a problem in week nine is only useful if it changes what you do in week one.

When the model shows a projected shortfall, the first question is: what's the lever? Collections are usually the fastest — accelerating a payment from a current client, offering a small early-pay discount, tightening the terms on a new engagement. Disbursements come second: which payables can move a week without a penalty or a relationship cost? Discretionary spend is third: what planned outlays can be pushed without consequence?

The forecast doesn't make those decisions for you. It makes them visible early enough that you have options. The owner who sees a tight week nine in week one can have three conversations before it's a problem. The owner who sees it in week eight has one.

The common objection: "our collections are too unpredictable"

Every business with a lumpy receivables book says this. The answer isn't to wait for a predictable business. It's to model the receivables conservatively — assume a percentage of what's on the aging will be late, and forecast against that assumption. The forecast is wrong, every week. That's fine. You update it, and you update your picture of what "wrong" usually looks like. Over time, you get better at predicting the lumpiness, which is most of what cash management is.

A forecast that is consistently wrong in the same direction is still useful — it tells you the bias in your assumptions. A forecast that surprises you in different directions every week is telling you something real about your collection pattern that instinct was smoothing over.

If your business is making decisions without a 13-week picture, that's usually the first thing we build when a new engagement starts. It takes one working session and an afternoon to get the first version running. A discovery call is the right place to start.